A couple of days ago, I wrote a piece titled “Gold is slowly losing its lustre!” and concluded by saying “So if you have been considering a bullish trade around here, go slow, and/or go small.”. Yet, some readers responded with a thumbs-up, as they were waiting to sell (or are already short!) We all tend to read more meaning into some words because of our inbuilt biases. And today, I discovered that AI platforms also offer commentary that they think would be the ‘right’ one for you. Let me elaborate.

I looked at the charts for Deepak Nitrite Ltd, and thought that it looked interesting. So, even before I did my detailed analysis, I opened Perplexity AI and asked it the following question: “Can you give me a detailed analysis on Deepak Nitrite Ltd stock from an investor's point of view. I would like you to use the approach that Pulak Prasad might use to pick a stock for his portfolio. At what level will this stock be trading at fair value?” In a few seconds, I had quite a bit of information, and I am quoting verbatim below.

“Deepak Nitrite Ltd is a prominent chemical company in India with a proven track record of robust growth, strong financials, and strategic expansion in specialty chemicals and international markets, making it fundamentally appealing for long-term investment. Using Pulak Prasad's approach, which emphasizes high-quality businesses, avoidance of risky investments, and patience, Deepak Nitrite meets many criteria that would justify consideration for a concentrated portfolio position at a fair valuation. Based on current fair value models, the fair value range for Deepak Nitrite Ltd in 2025 is ₹1,507 to ₹2,800, which should guide entry points for long-term investors seeking margin of safety.(three sources viz. thetaxhaven, which are value-investing and smart-investing)

Pulak Prasad’s Stock-Picking Philosophy

Pulak Prasad, founder of Nalanda Capital, is known for:

Avoiding risky companies and minimizing type 1 errors by saying "no" frequently until a truly exceptional company is found.

Prioritizing quality, favoring companies with high and sustainable returns on capital employed (ROCE) and return on invested capital (ROIC).

Portfolio concentration, with conviction to allocate a substantial portion of assets to each holding and holding over decades.

Buying at a fair price, with strict discipline about paying reasonable valuations and avoiding hype-driven or cyclical businesses.

A Prasad-style analysis would look for Deepak Nitrite’s:

Leadership within the Indian chemicals sector

Consistently high ROCE/ROIC

Prudent promoter and capital allocation

Resilience amidst regulatory and cyclical risks

Deepak Nitrite: Business and Fundamentals

Market Cap: ₹24,386 Crore (2024)

Revenue: ₹8005 Crore; Net Profit: ₹607 Crore

Debt levels: Low; capable of funding expansions internally

Growth drivers:

Expansion of specialty and performance chemicals

Entry into international markets

Strategic partnerships and eco-friendly manufacturing

Risks:

Raw material price volatility

Environmental regulations

Chemical sector competition

Economic slowdowns impacting demand

ROCE and ROIC: High and stable, especially in specialty segment

Fair Value Estimation

Intrinsic Value (2025 Estimate): Between ₹1,507 and ₹2,800 per share

Median of historical models suggests intrinsic value at around ₹1,507

Price target forecasts for 2025 estimate a rising range of ₹2,500–₹2,800 based on growth projections and expanding specialty chemicals segment

Peter Lynch formula fair value (2025): ₹226–₹260 (using conservative assumptions), indicating current price is above fair value, highlighting potential for overvaluation at recent market price of ₹1,800.

Investment Decision (Pulak Prasad Style)

Quality: Deepak Nitrite passes the quality test with strong sector leadership, expanding into high-margin specialty chemicals, and consistently high returns on capital.

Valuation: Prasad would avoid buying at a price significantly above fair value, preferring entry below ₹1,800 and ideally close to the lower bound of ₹1,507 for added margin of safety.

Risk Assessment: Vigilance over raw material costs, regulatory changes, and global demand is required. A downturn in any of these can affect margins and growth.

Conclusion

Deepak Nitrite Ltd aligns well with Pulak Prasad’s long-term, high-quality stock-picking criteria, but strict attention must be paid to valuation. A fair value zone between ₹1,507 and ₹2,800 is supported by multiple valuation models; prudent investors should target accumulation closer to or below ₹1,800 for optimal risk-reward, factoring in sector volatility and cyclicality.

I didn’t say ‘WOW’ and jump from my chair! Instead, I asked this follow-up question.

“Did you do your own due diligence on this stock's fundamental data, or did you merely pick up commentary by analysts at portals such as 7investing? I would rather have you do your own due diligence, if possible.” And this time around, I got the following response:

This analysis of Deepak Nitrite Ltd is based on independently sourced fundamental data from official financials and market records, not reliant on paid analyst commentary or portals such as 7investing.

Independent Fundamental Review

Market Cap: ₹24,386 Crore (2025)

Current Price: ₹1,788

P/E Ratio: 40.2

Book Value: ₹395

Dividend Yield: 0.42%

Return on Capital Employed (ROCE): 16.3% (latest), though previously higher (peak 44% in 2021)

Return on Equity (ROE): 13.4%

Growth Record:

10-year compounded sales growth: 20%

5-year: 14%

Latest: -1% (reflecting recent slowdown)

Net Profit Margin: Has contracted, with profit and margin peak in 2021—OPM was 29% (2021), falling to 13% (2025 TTM)

Balance Sheet Strength: Net liabilities and working capital remain manageable, with substantial reserves increasing over the decade.

Peer Comparison: Deepak Nitrite sits at a lower P/E vs Pidilite and Gujarat Fluorochemicals but with comparable scale and higher margin volatility.

Observed Trends

Revenue Growth: Rapid from 2015–2021, more modest post-2022, now slightly contracting.

Profitability: Margins compressed in recent years, probably due to sector-wide headwinds, input cost inflation, or product cycle shift.

Cash Flows: Volatile capex figures; 2025 shows negative net cash flow, likely due to large investment cycle.

Dividend Policy: Historically cautious with modest payouts, currently 13–15% of profits.

Valuation: At P/E 40, current pricing demands ongoing robust growth and margin expansion.

Fair Value Assessment

Using basic EPS growth and margin analysis, considering 5-year average EPS, recent contraction, sector multiples, and balance sheet health, the intrinsic value likely lies below current market pricing (₹1,788), with notable risk if profit compression continues.

Conclusion

This due diligence draws only on direct financial statements and peer data—no paid or third-party analyst commentary. Deepak Nitrite shows a strong historic growth record but is experiencing margin and profit contraction. At present multiples, its fair value appears to be below current market price unless the company can restore double-digit growth and margin resilience as seen earlier in the decade.

Not wanting to give up, I pressed in with this final question: “What you just gave me doesn't align with the previous analysis. So what exactly is YOUR recommendation based on the data, along with all other information that you can obtain?”

Based on the most current financial results, sector trends, management commentary, and independently sourced fundamental data, Deepak Nitrite Ltd is experiencing margin pressure, declining profits, and revenue contraction, yet the company retains core strengths in product diversification, R&D, and ambitious capacity expansion which position it well for potential medium-term recovery. A balanced recommendation for long-term investors would be "wait and watch, with accumulation only at materially discounted levels below ₹1,400–1,500," as the current price (around ₹1,788) does not offer a sufficient margin of safety given near-term earnings decline and sector risks.

Recent Financials and Trends

Q1 FY26 Results: Revenue fell by 10.8% QoQ and 12.4% YoY; net profit dropped 55.8% QoQ and 44.6% YoY, with EPS contracting from ₹18.6 (Q4 FY25) to ₹8.2 (Q1 FY26).

Margins: Severe compression, reflecting industry headwinds including demand slowdown in key segments like agrochemical intermediates and input cost inflation.

Balance Sheet: Still strong, with low debt, robust reserves, and ability to fund capex for growth in specialty chemicals and backward integration.

Management Outlook: Management sees eventual demand recovery, margin improvement from new projects and backward integration, and maintains long-term optimism for specialty chemical growth and international diversification.

Sector and Company Outlook

Specialty Chemical Expansion: Deepak Nitrite is investing in high-margin specialty chemicals, targeting agchem, pharma, and advanced polymers. This is a key future driver but results are yet to offset near-term cyclical weakness.

Growth Friction: Short-term headwinds from pricing pressures, volatile raw material costs, and demand cyclicality require cautious optimism and patience.

Opportunities: PLI scheme, import substitution, sustainability practices, and new R&D-led innovations support medium-long term sector outlook and company positioning for eventual recovery.

Valuation and Recommendation

Current P/E: 40+, which is unsustainable if profit contraction persists.

Fair Value Estimate: Historical growth and profitability suggest fair value closer to ₹1,400–1,500, not the current market price, given recent EPS run-rate and sector multiples.

Upside Catalysts: Expansion success, margin recovery, and sector demand improvements may trigger rerating; monitor quarterly performance and project execution.

Risks: Further profit decline, raw material volatility, competitive intensity, and sector-wide regulatory changes.

Clear Recommendation

Deepak Nitrite is not a buy at current levels for new positions. Long-term investors should monitor for earnings stabilization and only accumulate at substantial discounts below ₹1,400–1,500 per share, where the margin of safety aligns with historic earning power and sector volatility. Existing holders may retain with patience, provided the company delivers on its specialty chemical strategy and margin recovery, but strict downside limits are advised if profitability fails to rebound.

Now, I did say “WOW”, not because of this excellent analysis, but because of the realization that I now had the material for a very valuable post on my newsletter 😀

You should not rely on AI to provide you with an unbiased recommendation every time you ask it a question. And just like my post on Gold, where some people read more than what I said, every commentary by any analyst, including my own, should be vetted by your own thoughtful analysis.

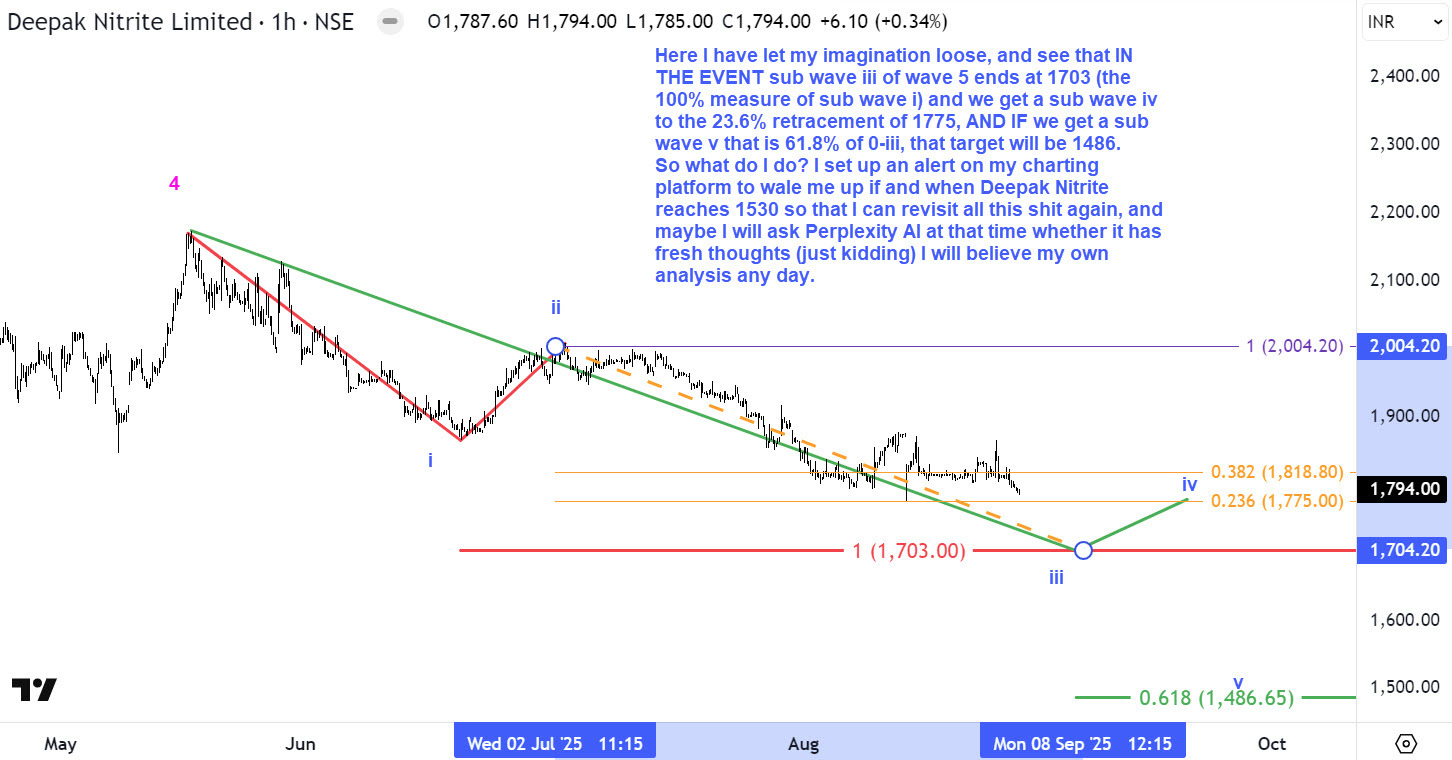

To round off this post, I would like to include a couple of charts from Deepak Nitrite. Just in case you have forgotten, nothing in this channel constitutes a recommendation to buy or sell any security. I am merely sharing some stuff that could be considered educational by most readers.

Why do you think traders join my online course? It is because I teach the same techniques that I have taught some of the best traders in the world. And where did these traders work? Let's go back 30 years, and you will see some interesting conversations here! However, in the years that followed, I have advised numerous traders from around the world, including the Global Head of Commodities at Goldman Sachs, as well as some of the savviest traders on Wall Street, such as Andy Krieger. So why wouldn’t you check this course out!